![]() 15

15

How a Fintech Company Automated 70% of Customer Queries Using a Custom GenAI Chatbot

![]() 5 min read

5 min read

![]() 15

15

![]() 5 min read

5 min read

20%

Execs who'd trust AI alone with a financial transaction

22-94%

Model hallucination rate on user-framed false claims

80% by 2029

Service issues Gartner predicts agentic AI resolves by 2029

A headline like “automated 70% of customer queries” tends to hide more than it shows. Seventy percent of what, though? Genuinely resolved, or just shoved somewhere else? In fintech, where a wrong answer can turn into a compliance event rather than a one-star review, that difference is the entire story.

So here’s this one straight. A mid-sized fintech client came to us drowning in support volume, and we built them a custom generative AI chatbot for fintech support that now handles around 70% of their incoming queries. But the interesting part isn’t the number. It’s how we got there, which was less about a clever model and more about teaching the bot, very deliberately, when to shut up and fetch a human. As a piece of customer service automation, it’s a useful case of what the work actually takes when the margin for error is thin.

The client ran a popular consumer finance app. Their support team was buried: thousands of tickets a week, most of them the same handful of questions, answered the same way, over and over. Response times were creeping up, the team was burning out on repetitive work, and hiring more agents just to field “where’s my transfer” felt like the wrong answer.

An off-the-shelf chatbot was tempting, and they’d looked at a few. The problem is that fintech is a uniquely unforgiving place to put a generative model. In most industries, a hallucinated answer is an annoyance. In finance, it can be a regulatory finding, a leaked piece of personal data, or a customer making a financial decision on wrong information. Independent testing on leading models has found hallucination-type failure rates as low as 22% and as high as 94%, depending on how a false claim is framed, and models can distort facts even when handed the correct source document. That’s not a risk you wave through.

Then there are the obligations a generic bot was never built to meet. PCI DSS says card numbers and account details have to be caught and stripped before they ever reach a model. SOC 2 and GDPR set their own bars. Personal data has to be redacted in the moment, not tidied up afterward, and every single thing the system says or does has to be logged so it can be reconstructed later. The client didn’t need a chatbot that could talk. They needed one that could be trusted and then proven trustworthy when someone came asking. So they skipped the plug-in tools and wanted a custom build from a generative AI development company that had lived inside regulated industries before and knew what an auditor would eventually want to see.

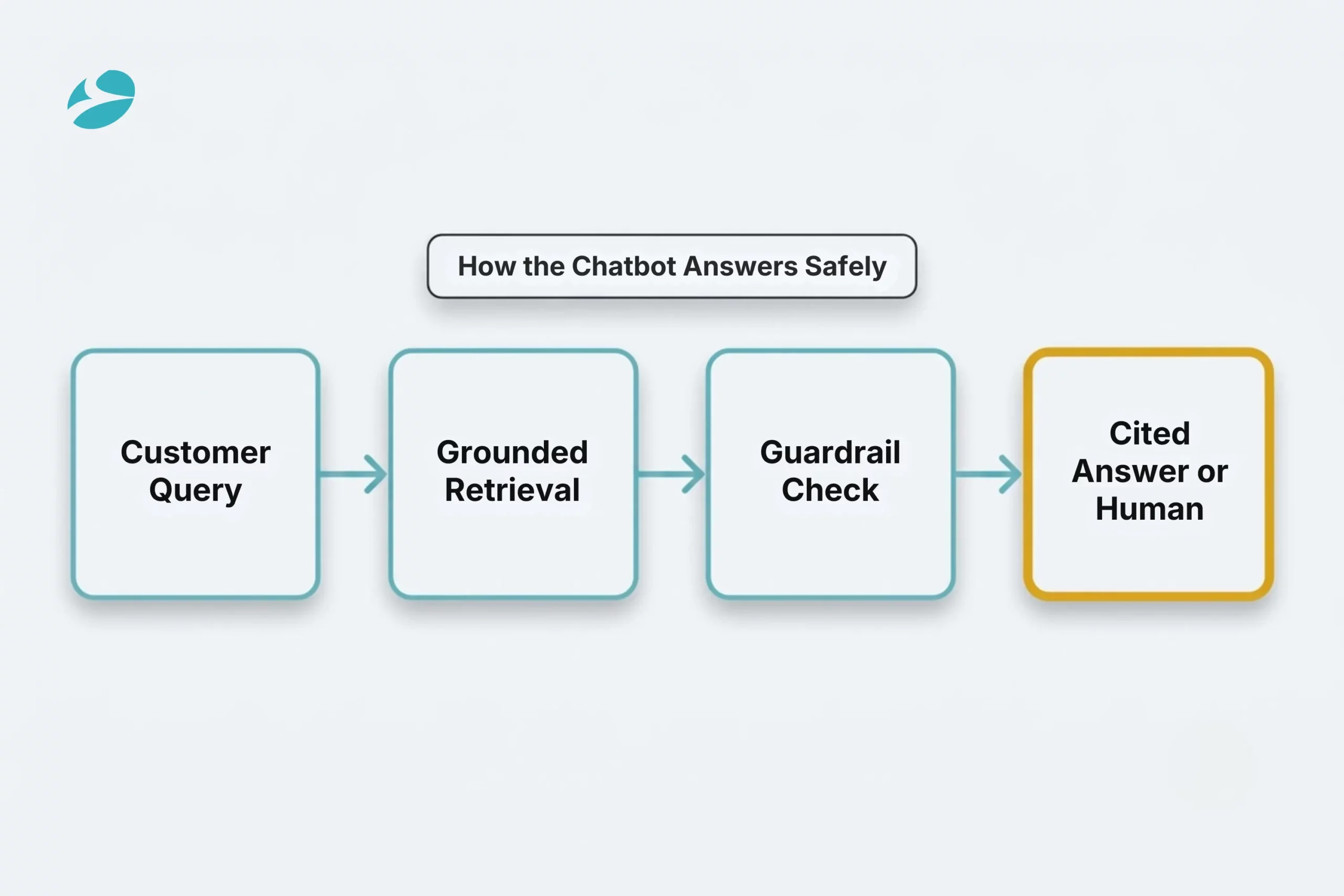

We didn’t build a model that knows about finance. We built a system that only ever answers from the client’s own vetted material, and that knows when it’s out of its depth.

At the center sits retrieval-augmented generation, or RAG. Before the chatbot says a word, it goes and finds the relevant passages in the client’s own approved material, the help center, the policy pages, the product docs, old resolved tickets, and then answers only from what it pulled back, with a link to the source. That link earns its keep twice over. It reassures the customer, and it gives compliance the audit trail it needs. The model isn’t reciting finance from memory. It’s reading the client’s current, approved answers and passing them along.

Around that core, we built the part that actually makes it safe for fintech:

The build ran in a deliberate order. We mapped the highest-volume query types first, then grounded the model in vetted content. The guardrails and escalation paths came next, designed up front instead of bolted on after the fact. Only then did we wire it into the support desk and the core systems, test it hard for accuracy and for compliance, and roll it out in phases with one eye always on the numbers. That order is not incidental. In fintech, the escalation logic isn’t a feature you tack on once a bad answer shows up in production. It’s the foundation you pour first.

This is the part most case studies skip, so here’s the honest accounting.

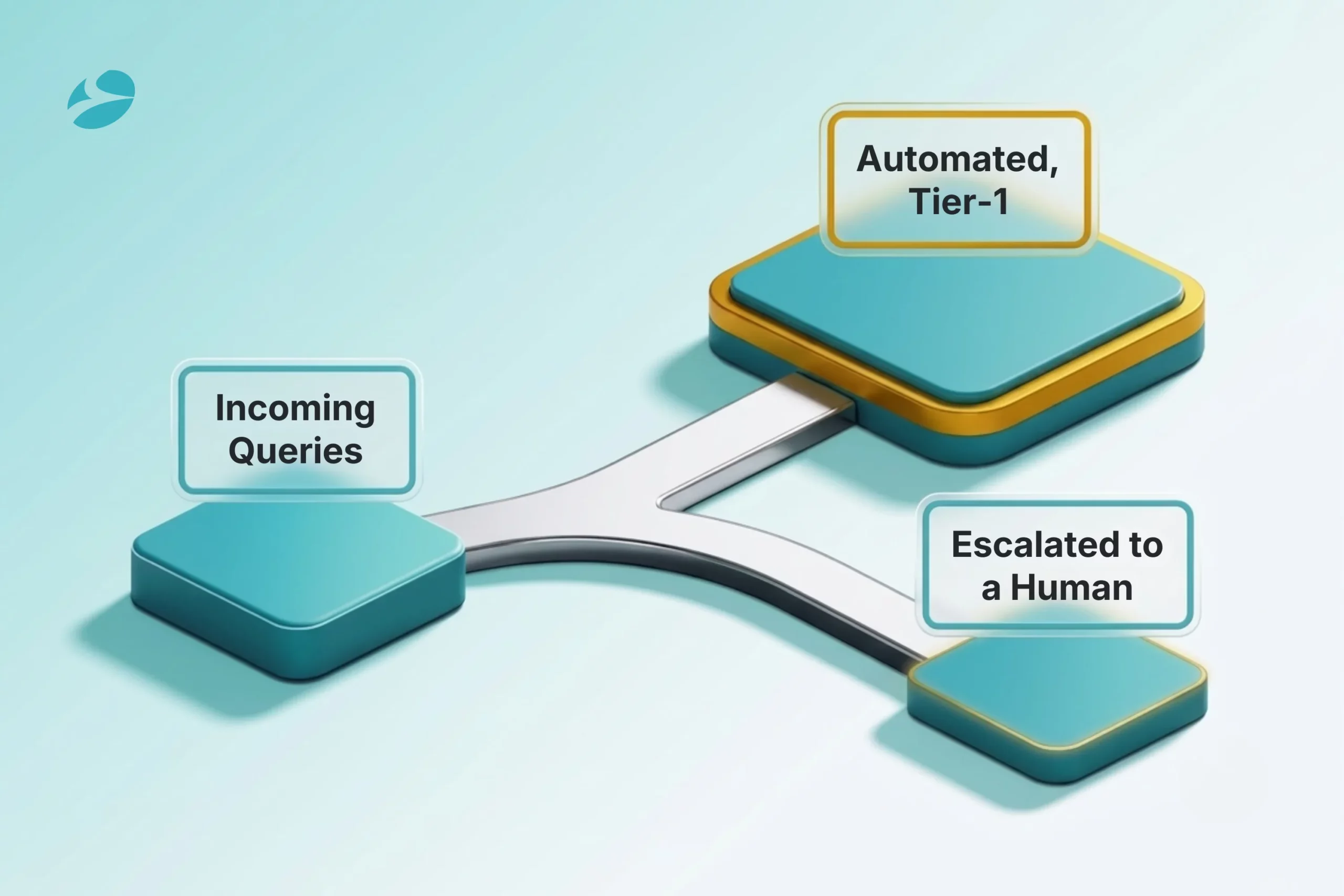

“Automated 70%” does not mean the bot fields 70% of everything a customer might ask. Marketing tends to blur three very different numbers. Containment is just the share of chats that stay in-channel. Deflection is the share that never reaches a human and actually gets a useful answer. True resolution is the problem genuinely solved, end-to-end. A bot can happily “contain” a conversation with a reply that helps nobody. It was that third number we cared about.

So the 70% here is top-query containment on tier-1 intents, and that’s the honest, credible target. Independent research backs up the caution: only 20% of business executives say they would trust an AI agent to handle a financial transaction on its own. Landing well above that bar came down to grounding and guardrails, not wishful thinking.

What the chatbot handles well is the high-volume, low-ambiguity work: balance and transaction checks, statement requests, card actions like activation and lost-card replacement, password resets and account recovery, contact-detail updates, and transfer status. These are the questions that made up the bulk of the queue, which is exactly why automating them moved the needle.

What we deliberately left to humans is the other side of the same coin: disputes, anything resembling financial advice, suspected fraud, and credit decisions. We didn’t fail to automate these. We chose not to because they carry the kind of risk where “mostly right” isn’t good enough. That choice is the design, not a limitation of it. The 70% exists because the bot is allowed, and encouraged, to say “let me get a colleague who can help with that.”

A few months past the phased rollout, the picture was clear enough. Roughly 70% of incoming tier-1 queries were getting resolved by the chatbot with no human involved, at any hour, in seconds instead of minutes or hours. The support team didn’t get smaller. It moved. Off the treadmill of “where’s my transfer,” agents shifted to the knotty, judgment-heavy cases that actually need a person, and oddly, the job got more satisfying, not less. On the automated queries, response time basically fell to nothing, and the human queue behind them grew shorter and a lot calmer.

The money side followed. An automated query cost a sliver of a human-handled one, and since the bot never slept, the client stopped paying overtime and night cover just to keep response times bearable. Satisfaction with those automated intents actually went up. Not because a bot is warmer than a person, but because a correct, cited answer at two in the morning beats waiting four hours for the same fact. And when traffic spiked, the system just took it, whereas a year before, that same surge meant a panicked round of hiring.

The thing that made it work wasn’t the model. Good models are increasingly a commodity. What made it work was the discipline around the model: grounding every answer in vetted content, tuning the system to escalate when uncertain, and drawing a hard line around the intents that must stay human. In a regulated business, a customer service automation project lives or dies on that discipline. A chatbot that’s confidently wrong 5% of the time isn’t 95% helpful in fintech; it’s a liability with good uptime.

If one lesson is worth carrying away from this, it’s that the automation rate is a byproduct, not a target. We never chased 70%. We built a system that was honest about what it didn’t know, and 70% is just what was left over once it stopped guessing.

1

It shouldn’t, and a well-built one won’t even try. Disputes, financial advice, suspected fraud, and credit decisions, these carry far too much risk for an automated answer, so the right design sends them straight to a person, no matter how sure the model sounds. Automating the safe, high-volume stuff while deliberately escalating the sensitive stuff is the whole point, not a shortcoming.

2

It takes three things working together. First, ground every answer in the company’s vetted content with RAG, so the bot hands back approved material and a citation instead of inventing from memory. Second, put a guardrail layer in front and set the confidence bar high, because raw model confidence can’t be trusted on its own. Third, escalate to a human the moment the system is unsure. Grounding plus deliberately pessimistic guardrails are what keep a finance chatbot honest.

3

It can be, as long as compliance is built in from day one rather than discovered at the end. In practice, that means stripping personal and card data in real time before it reaches the model, checking identity before any account action, logging every interaction for audit, and staying in control of where the data is processed. Compliance is an architectural decision, never a switch you flip later.

4

The high-volume, low-ambiguity ones. Think balance and transaction checks, statements, card activation or replacement, password resets, account recovery, a contact-detail change, and a transfer status. That cluster is usually the bulk of the queue, which is why automating it has an outsized effect even while the sensitive cases stay firmly with people.

5

It varies with how much content there is, how many integrations there are, and how wide the compliance scope is. But the sensible path doesn’t change. Start with a tight pilot on a few high-volume, low-risk intents, prove the containment and the safety there, then widen out. Phasing it like that gets real value into production sooner and keeps the risk boxed in, instead of gambling everything on a big-bang launch.